r&d tax credit calculation example

This is allowable for tax purposes and would generate an RD tax credit up to 33 of each years deductible costs 66k in each year. The RD tax credit is complicated for firms to claim and smaller firms sometimes have a hard time accessing the credit.

The Earned Income Tax Credit Eitc Legislative History Everycrsreport Com

67-275 at 17 1921 describing the need to avoid Start Printed Page 285 allowing a foreign tax credit to wipe out tax properly attributable to US.

. Before April 1 2015 and after March 31 2012 the Saskatchewan tax credit was refundable for CCPCs subject to a 3 million expenditure limit and non-refundable in all other. RD Tax Credit Calculation. The economic literature on the RD tax credit suggests that it increases RD spending although the magnitude of that increase and how much of that new research translates to new innovation is more ambiguous.

For example software companies that invest in their technology. Conversely if an amount would have been included in your assessable income under the standard balancing adjustment provision of section 40-285 the sum of that amount the section 40-285 amount plus an additional amount is included in your assessable income. See for example S.

For the other corporations the Saskatchewan RD tax credit remains a non-refundable tax credit at the rate of 10 on eligible expenditures incurred after March 31 2015. Generally businesses can claim RD tax credits for tax returns with an open statute of limitations which typically includes the prior three years. Before you can calculate the amount you receive in RD tax credit carryforward youll need to ensure that your business is located in the US and pays tax.

Due to it being simple to understand it is often called an alternative simplified credit. Your RD tax credit is not taxable income. If you qualify you can file an RD Tax Credits claim each yearThe benefit you will receive will be a portion of your qualifying expenditure how much you have spent on activities that are considered RD for tax.

By logging payment dates notes regarding those payments and any questions you may have at that moment in time youll ease the process and make taxes more manageable for everyone. 1 2008 or earlier all gains under a 2013 installment sale escape the BIG tax even if the 10-year recognition period springs into. It is a below-the-line benefit and will be shown in your income statement also known as your profit-and-loss account either as a Corporation Tax reduction or a credit.

100k of qualifying RD expenditure is spent by a business on developing a software platform. Some tax treatment is slightly modified from the rules under the consolidated tax regime. On the other hand the research and development RD tax credit and foreign tax credit will be calculated on a group-wide basis and the creditable amount will be allocated to member corporations based on the respective corporate tax liabilities.

That notional RD deduction is included in the calculation of your RD tax offset. On Finance 98th Cong 2d Sess Deficit Reduction Act of 1984 Explanation of Provisions Approved by the Committee on March 21. The treatment of all gain recognized under the installment method for BIG tax purposes is governed by the BIG tax provisions in effect for the year of sale.

Amortised over 5 years 20k would be charged to the income statement each year. How far back can you claim RD tax credits. We can then subtract the 5000 shares repurchased from the 10000 new securities created to arrive at 5000 shares as the net dilution ie the number of new shares post-repurchase.

Since these taxpayers are under the threshold amount the only. The RD tax credit is an example of a carryforward credit. The RD tax credit scheme is a UK government scheme that is aimed at rewarding and incentivising innovation in the private sector.

Treasury Stock Method Calculation of Diluted Shares. For instance lets say that a company has 100000 common shares outstanding and 200000 in net income in the last twelve months. 21 For example if the S election was effective on Jan.

For SMEs claiming RD tax credits the accounting treatment is straightforward. A married couple filing jointly have 300000 of taxable income and a business that is an SSTB with 225000 of QBI before considering 125000 of W-2 wages paid to the shareholderemployee. This estimated quarterly tax payment calculator isnt just for conveying information with your tax expert but also for communicating with your future self.

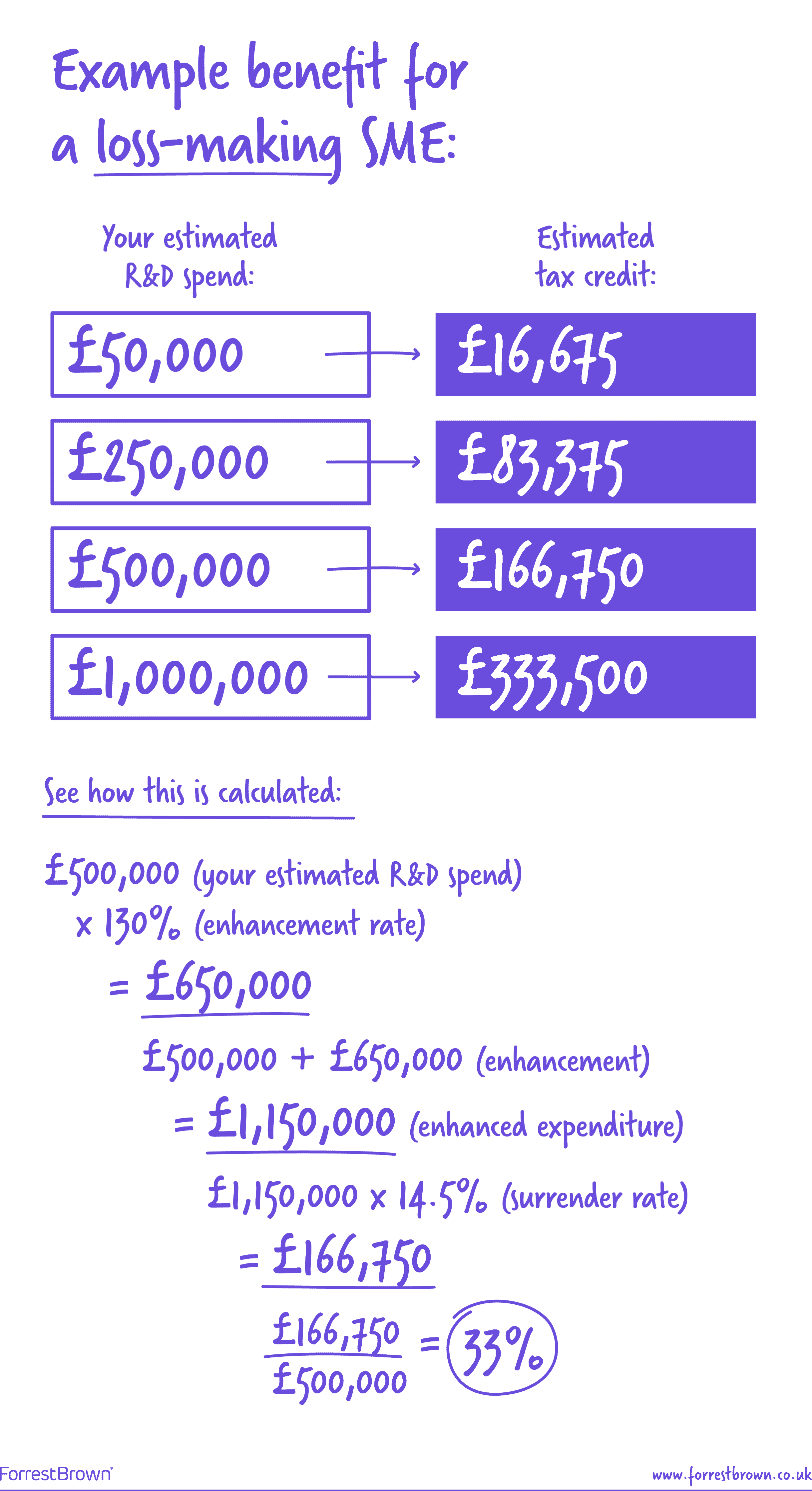

SSTB using an S corporation under the threshold amount. Accounting treatment for SME RD tax credit scheme.

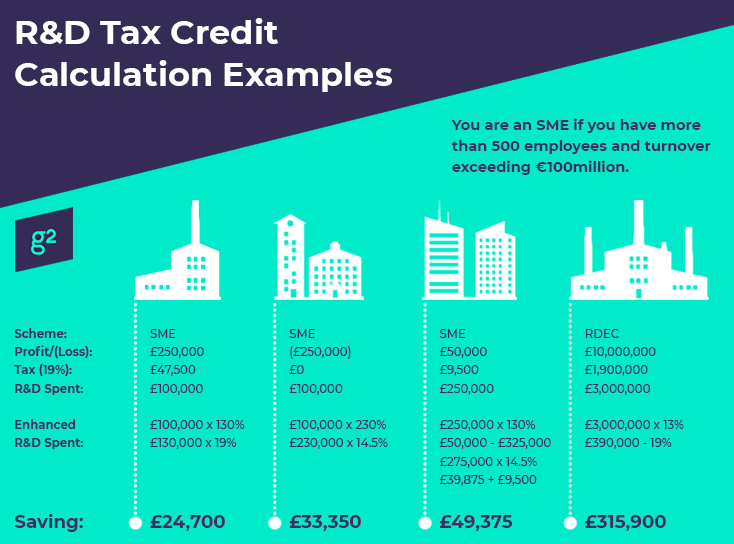

R D Tax Credit Calculation Examples Mpa

Taking The Credit Tax Adviser

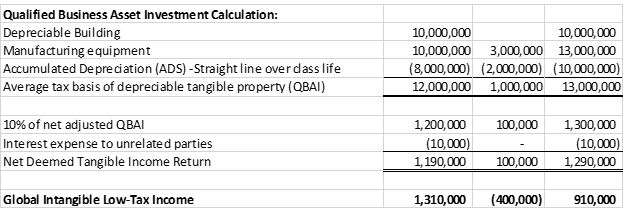

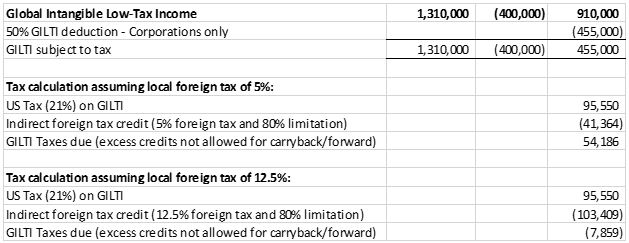

Global Intangible Low Tax Income Working Example Executive Summary Mksh

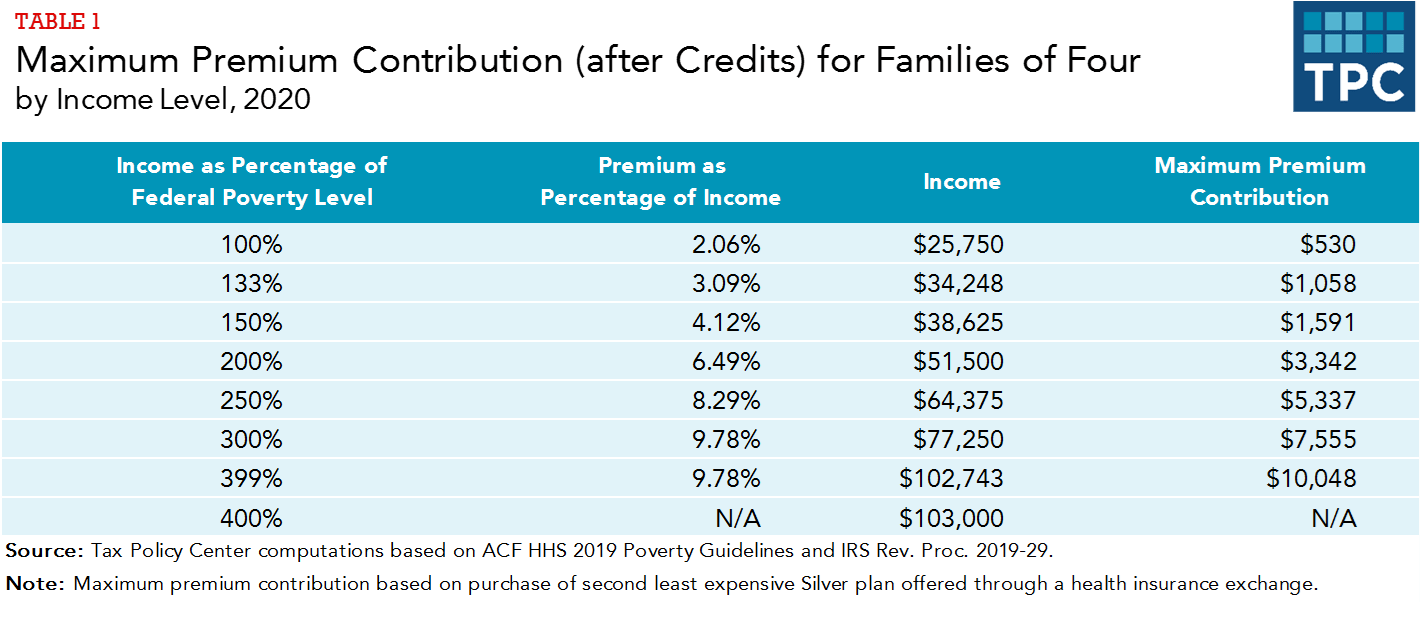

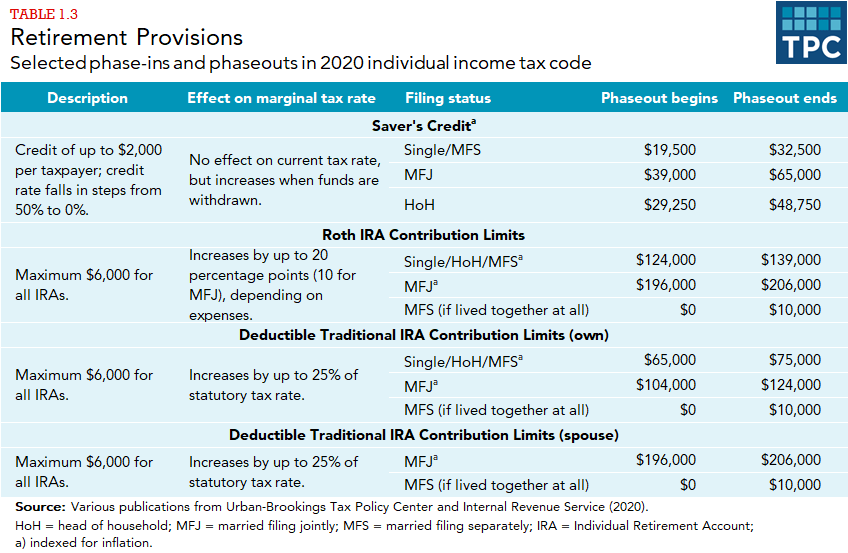

What Are Premium Tax Credits Tax Policy Center

State R D Tax Credits Are You Missing Out Wipfli

Rdec Scheme R D Expenditure Credit Explained

Global Intangible Low Tax Income Working Example Executive Summary Mksh

R D Tax Credit Calculation Examples Mpa

R D Tax Credit Calculation Examples Mpa

R D Tax Credit Calculation Methods Adp

R D Tax Credits Calculation Examples G2 Innovation

The R D Tax Credit Aspects Of Saas Start Ups R D Tax Savers

The Amt And The Minimum Tax Credit Strategic Finance

R D Tax Credit Calculation Methods Adp

R D Tax Credit Rates For Sme Scheme Forrestbrown

How Do Phaseouts Of Tax Provisions Affect Taxpayers Tax Policy Center

Why Research Funding Sources Complicate Tax Credits Research Development World

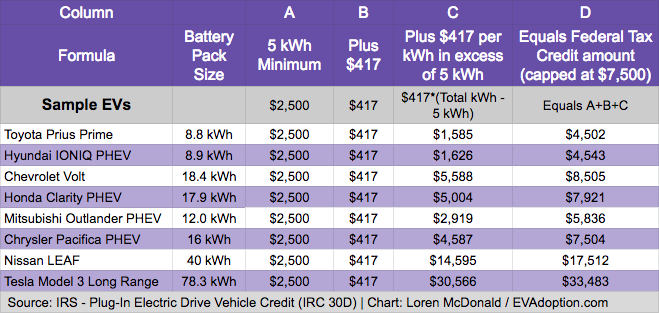

How The Federal Ev Tax Credit Amount Is Calculated For Each Ev Evadoption

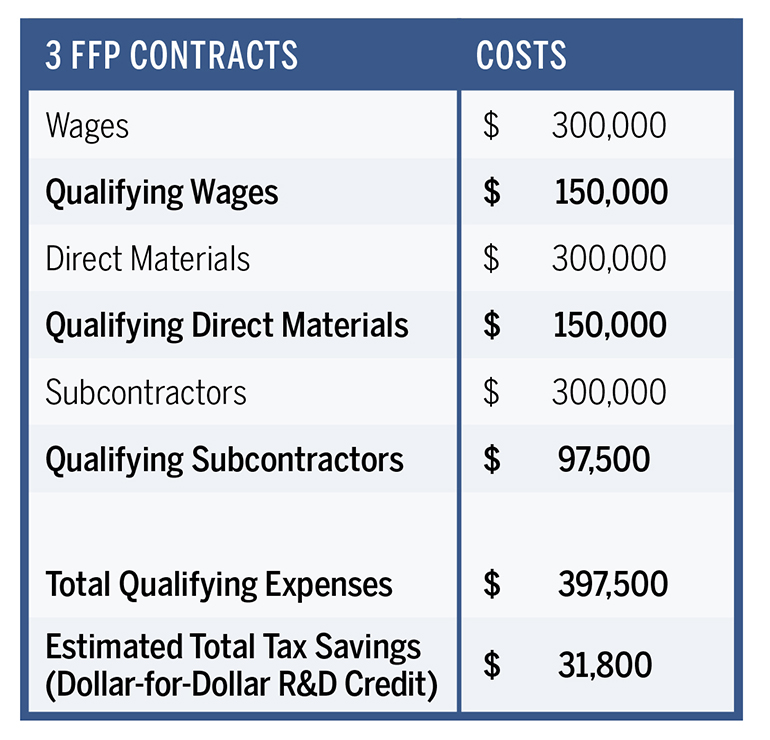

R D Tax Credit Calculation Examples Mpa